Người nộp thuế mới hoạt động có được chọn xoilac tv trực tiếp bóng đá hôm nay thuế giá trị gia

May new businesses declare value-added trực tiếp bóng đá euro hôm nay quarterly in Vietnam?

Pursuant to Point a, Clause 1, Article 9 ofDecree 126/2020/ND-CP, the quarterly VAT declaration applies to:

- Taxpayers required to file monthly VAT returns as stipulated in Point a, Clause 1, Article 8 ofDecree 126/2020/ND-CPwho have a total revenue from sales of goods and services in the preceding year of 50 billion VND or less can declare VAT quarterly. The revenue from sales and services is determined as the total revenue on VAT returns for trực tiếp bóng đá euro hôm nay calculation periods within the calendar year.

In cases where taxpayers file consolidated trực tiếp bóng đá euro hôm nay returns at the main headquarters for dependent units or business locations, the revenue from sales and services includes the revenue of such dependent units or business locations.

- For taxpayers newly commencing business operations, they are allowed to choose to declare VAT quarterly. After engaging in business operations for a full 12 months, from the next calendar year after the 12 months, they will determine their VAT declaration basis according to the revenue level of the previous calendar year (for a full 12 months) by either monthly or quarterly trực tiếp bóng đá euro hôm nay periods.

Therefore,according to the regulation, new businesses can choose to declare VAT quarterly.

If, after conducting business for a full 12 months, from the next calendar year after the full 12 months, they will base the decision on the revenue of the previous calendar year (for a full 12 months) to declare VAT monthly or quarterly.

May new businesses declare value-added trực tiếp bóng đá euro hôm nay quarterly in Vietnam?(Image from the Internet)

Vietnam: What is the deadline for submitting the VAT return for the fourth quarter of 2024?

Based on Article 44 of theLaw on trực tiếp bóng đá euro hôm nay Administration 2019, the deadline for submitting trực tiếp bóng đá euro hôm nay returns is regulated as follows:

- The deadline for submitting trực tiếp bóng đá euro hôm nay returns for taxes filed monthly or quarterly is as follows:

+ For monthly declaration and submission, it is no later than the 20th day of the month following the month in which the trực tiếp bóng đá euro hôm nay obligation arises.

+ For quarterly declaration and submission, it is no later than the last day of the first month of the quarter following the quarter in which the trực tiếp bóng đá euro hôm nay obligation arises.

- The deadline for submitting trực tiếp bóng đá euro hôm nay returns for taxes calculated on an annual basis is regulated as follows:

+ No later than the last day of the third month from the end of the calendar or fiscal year for annual trực tiếp bóng đá euro hôm nay finalization returns; no later than the last day of the first month of the calendar or fiscal year for annual trực tiếp bóng đá euro hôm nay returns;

+ No later than the last day of the fourth month from the end of the calendar year for personal income trực tiếp bóng đá euro hôm nay finalization returns for individuals who directly finalize taxes;

+ No later than December 15 of the previous year for presumptive trực tiếp bóng đá euro hôm nay returns for business households and individual businesses paying trực tiếp bóng đá euro hôm nay by presumptive method; in case of newly established business households or individual businesses, the deadline for submitting presumptive trực tiếp bóng đá euro hôm nay returns is no later than 10 days from the commencement of business.

Therefore,according to these regulations, the deadline for submitting the VAT return for the fourth quarter of 2024 is no later than January 31, 2025.

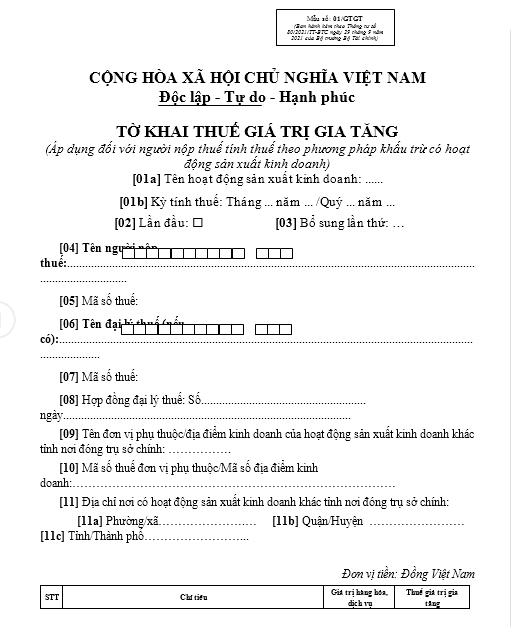

What is the form for the VAT return for the fourth quarter of 2024 in Vietnam?

Accordingly, the VAT return for the third quarter of 2024 is made according to the form in the Appendix issued withCircular 80/2021/TT-BTCas follows:

Download the VAT return form for the fourth quarter of 2024.

What are cases where businesses must declare VAT returns in Vietnam?

According to the provisions of Article 3 ofCircular 219/2013/TT-BTC, businesses and business households are required to file and pay VAT if they are engaged in production, trading of goods, and services subject to VAT in Vietnam, irrespective of industry, type, form of business organization or businesses, and business households importing goods, purchasing services from overseas subject to VAT, specifically:

- Enterprises and business households established and registered under the Law on Enterprises 2020 and other specialized business legislation.

- Enterprises with foreign invested capital and foreign parties participating in business cooperation contracts under the Law on Investment 2020.

- Enterprises and business households operating and trading in Vietnam acquiring services (including services associated with goods) from foreign organizations without permanent establishments in Vietnam, individuals residing outside Vietnam being non-resident subjects, shall be liable for VAT, except for cases exempt from declaring, calculating and paying VAT mentioned in Section 2 below.

- Branches of export processing enterprises established to engage in goods trading and activities directly related to goods trading in Vietnam as prescribed by laws on industrial parks, export processing zones, and economic zones.