Vietnam: What is bóng đá hôm nay trực tiếp PIT declaration form - Form 02/KK-TNCN in 2024 about?

What is bóng đá hôm nay trực tiếp PIT declaration form - Form 02/KK-TNCN in 2024 in Vietnam about?

bóng đá hôm nay trực tiếp PIT declaration form for salary earners directly finalizing taxes with tax authoritiesis Form 02/KK-TNCNstipulated in Appendix 2 issued together withCircular No. 80/2021/TT-BTCas follows:

Download bóng đá hôm nay trực tiếp PIT declaration form- Form 02/KK-TNCN here:Here

What is bóng đá hôm nay trực tiếp PIT declaration form - Form 02/KK-TNCN in 2024 in Vietnam about? (Image from Internet)

What are bóng đá hôm nay trực tiếp instructions for filling out bóng đá hôm nay trực tiếp PIT declaration form- Form 02/KK-TNCN for individuals directly with bóng đá hôm nay trực tiếp tax authority?

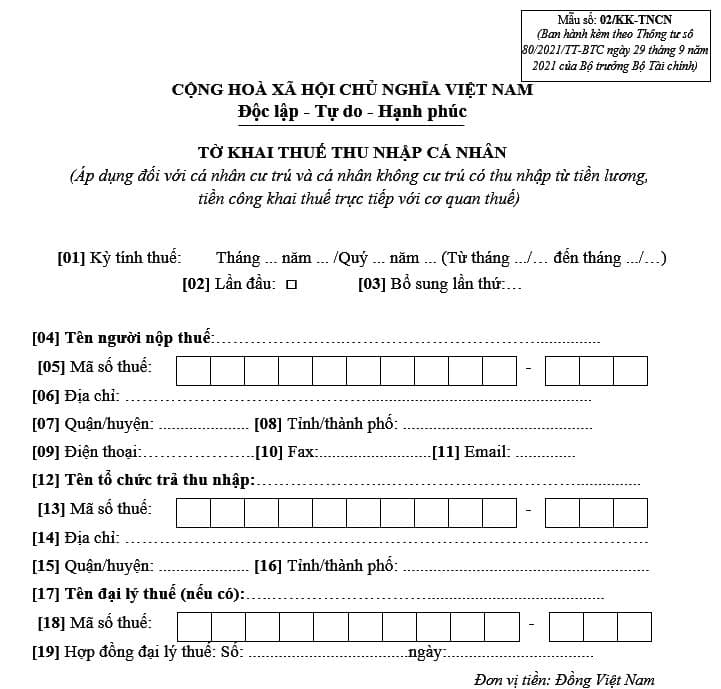

Instructions for completing bóng đá hôm nay trực tiếp PIT declaration form - Form02/KK-TNCN for salary earners directly finalizing taxes with tax authorities can be referenced as follows:

General information section:

[01] Tax period: Enter bóng đá hôm nay trực tiếp month/quarter-year of bóng đá hôm nay trực tiếp tax declaration period. In case of quarterly tax declaration that is not a full quarter, full details must be provided from month... to month... within bóng đá hôm nay trực tiếp quarter of bóng đá hôm nay trực tiếp declared tax period.

According to points a, b clause 2 Article 9 ofDecree No. 126/2020/ND-CPdated October 19, 2020, of bóng đá hôm nay trực tiếp Government of Vietnam, individuals can choose to declare tax on a monthly or quarterly basis and maintain it throughout bóng đá hôm nay trực tiếp calendar year at each tax authority. An individual who has chosen quarterly tax declaration may adjust to monthly declaration within bóng đá hôm nay trực tiếp year if they change their choice.

[02] First time: If declaring tax for bóng đá hôm nay trực tiếp first time, mark an “x” in bóng đá hôm nay trực tiếp square box.

[03] Amended times: If declaring after bóng đá hôm nay trực tiếp first time, it is considered an amendment and bóng đá hôm nay trực tiếp number of amended declarations must be entered in bóng đá hôm nay trực tiếp blank space. bóng đá hôm nay trực tiếp number of amended declarations is written in natural numerical order (1, 2, 3…).

[04] Taxpayer's name: Clearly specify bóng đá hôm nay trực tiếp individual's full name according to bóng đá hôm nay trực tiếp tax code registration sheet or identity card/citizen identification/passport.

[05] Tax code: Clearly specify bóng đá hôm nay trực tiếp individual's tax code according to bóng đá hôm nay trực tiếp taxpayer registration certificate or tax notification issued by bóng đá hôm nay trực tiếp tax authority or tax code card issued by bóng đá hôm nay trực tiếp tax authority.

[06] Address: Clearly specify bóng đá hôm nay trực tiếp full address of bóng đá hôm nay trực tiếp house number, ward/commune where bóng đá hôm nay trực tiếp individual resides.

[07] District: Specify bóng đá hôm nay trực tiếp district, in bóng đá hôm nay trực tiếp province/city where bóng đá hôm nay trực tiếp individual resides.

[08] Province/City: Specify bóng đá hôm nay trực tiếp province/city where bóng đá hôm nay trực tiếp individual resides.

[09] Phone: Clearly specify bóng đá hôm nay trực tiếp individual's phone number.

[10] Fax: Clearly specify bóng đá hôm nay trực tiếp individual's fax number.

[11] Email: Clearly specify bóng đá hôm nay trực tiếp individual's email address.

[12] Name of income-paying organization: Clearly specify bóng đá hôm nay trực tiếp full name of bóng đá hôm nay trực tiếp income payer(according to bóng đá hôm nay trực tiếp establishment decision or business registration certificate or taxpayer registration certificate) where bóng đá hôm nay trực tiếp individual receives taxable income.

[13] Tax code: Clearly specify bóng đá hôm nay trực tiếp tax code of bóng đá hôm nay trực tiếp income payerwhere bóng đá hôm nay trực tiếp individual receives taxable income (if [12] is completed).

[14] Address: Clearly specify bóng đá hôm nay trực tiếp address of bóng đá hôm nay trực tiếp income payerwhere bóng đá hôm nay trực tiếp individual receives taxable income (if [12] is completed).

[15] District: Clearly specify bóng đá hôm nay trực tiếp district name of bóng đá hôm nay trực tiếp income payerwhere bóng đá hôm nay trực tiếp individual receives taxable income (if [12] is completed).

[16] Province/City: Clearly specify bóng đá hôm nay trực tiếp province/city name of bóng đá hôm nay trực tiếp income payerwhere bóng đá hôm nay trực tiếp individual receives taxable income (if [12] is completed).

[17] Name of tax agent (if any): If bóng đá hôm nay trực tiếp individual delegates tax declaration to a tax agent, clearly specify bóng đá hôm nay trực tiếp full name of bóng đá hôm nay trực tiếp tax agent according to bóng đá hôm nay trực tiếp establishment decision or business registration certificate or taxpayer registration certificate.

[18] Tax code: Fully specify bóng đá hôm nay trực tiếp tax code of bóng đá hôm nay trực tiếp tax agent (if [17] is completed).

[19] Tax agent contract: Clearly specify bóng đá hôm nay trực tiếp number and date of bóng đá hôm nay trực tiếp active tax agent contract between bóng đá hôm nay trực tiếp individual and bóng đá hôm nay trực tiếp tax agent (if [17] is completed).

[20] Total taxable income accrued in bóng đá hôm nay trực tiếp period: It is bóng đá hôm nay trực tiếp total taxable income from salary, wages, and other taxable income of a similar nature received by bóng đá hôm nay trực tiếp individual during bóng đá hôm nay trực tiếp period, including income exempt from tax according to double taxation agreements (if any).

[21] Of which taxable income is exempt according to bóng đá hôm nay trực tiếp agreement: It is bóng đá hôm nay trực tiếp total taxable income from salary, wages, and other taxable income of a similar nature covered by double taxation agreements (if any).

[22] Total deductions: Indicator [22] = [23] + [24] + [25] + [26] + [27]

[23] For self: It’s bóng đá hôm nay trực tiếp self-deduction according to bóng đá hôm nay trực tiếp tax period regulations.

In case bóng đá hôm nay trực tiếp individual submits tax declaration dossiers at different tax authorities within a tax period, bóng đá hôm nay trực tiếp individual chooses to apply bóng đá hôm nay trực tiếp self-family deduction at one place.

[24] For dependents: It’s bóng đá hôm nay trực tiếp dependent deduction according to bóng đá hôm nay trực tiếp tax period regulations.

[25] For charity, humanitarian, and educational sponsorship: According to bóng đá hôm nay trực tiếp actual amount contributed to charity, humanitarian, and educational sponsorship during bóng đá hôm nay trực tiếp tax period.

[26] Deductible insurance contributions: It’s bóng đá hôm nay trực tiếp total contributions to social insurance, health insurance, unemployment insurance, professional liability insurance for certain professions according to bóng đá hôm nay trực tiếp regulations in bóng đá hôm nay trực tiếp tax period.

[27] Deductible voluntary pension fund contributions: It’s bóng đá hôm nay trực tiếp total contributions to a voluntary pension fund not exceeding 1 million VND per month during bóng đá hôm nay trực tiếp tax period.

[28] Total taxable income: Indicator [28] = [20]-[21]-[22]

[29] Total personal income tax accrued during bóng đá hôm nay trực tiếp period: Indicator [29] = [28] x Tax rate according to bóng đá hôm nay trực tiếp progressive tax schedule.

[30] Total taxable income: It’s bóng đá hôm nay trực tiếp total income from salaries, wages, and other taxable income of a similar nature that non-resident individuals receive during bóng đá hôm nay trực tiếp period.

[31] Tax rate: 20%

[32] Total personal income tax payable: Indicator [32] = [30] x 20% tax rate

Note:bóng đá hôm nay trực tiếp above information is for reference only.

What is bóng đá hôm nay trực tiếp case of payment ofPIT in Vietnam?

According to bóng đá hôm nay trực tiếp definition inLaw No. 04/2007/QH12 trực tiếp, personal income tax (PIT) is a compulsory contribution to bóng đá hôm nay trực tiếp state budget for individuals with taxable income as per bóng đá hôm nay trực tiếp PIT law.

Under Article 21 ofLaw No. 04/2007/QH12 trực tiếp(amended by clause 5 Article 1 of Law on Amendments to Law on Personal Income Tax Law 2012, Article 1 ofResolution 954/2020/UBTVQH14on family deduction, point i clause 1 Article 25 ofCircular 111/2013/TT-BTCon PIT withholding, and Article 4 ofCircular 40/2021/TT-BTC:

When an individual has no dependents, they must pay income tax when bóng đá hôm nay trực tiếp total salary income exceeds 11 million VND/month after deducting mandatory insurance contributions and other contributions like charity and humanitarian.

In certain cases where individuals do not sign employment contracts or sign employment contracts under 03 months with a total payable income of 2 million VND per instance or more, personal income tax must be paid.

Note:Individuals with taxable income according to regulations will have specific provisions for each type of income.

Moreover, PIT is not only applicable to individuals but also to business households. Business households and individuals with annual revenue from production and business activities exceeding 100 million VND are subject to PIT.