What are guidelines for filling in Item 23 on xem bóng đá trực tiếp nhà cái Form 01/GTGT - VAT Declaration in Vietnam?

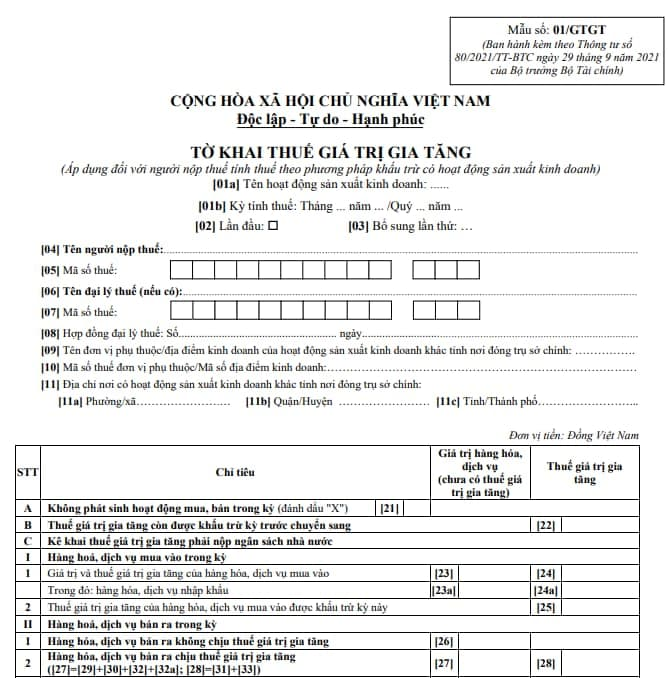

What is xem bóng đá trực tiếp nhà cái Form01/GTGT for VAT Declaration in Vietnamunder Circular 80?

xem bóng đá trực tiếp nhà cái latest VAT declaration form is stipulated in Form 01/GTGT in Appendix 2 issued along withCircular 80/2021/TT-BTCas follows:

Download VAT Declaration Form 01/GTGT:Here

What are guidelines for filling in Item 23 on xem bóng đá trực tiếp nhà cái Form 01/GTGT - VAT Declaration in Vietnam? (Image from xem bóng đá trực tiếp nhà cái Internet)

What are guidelines for filling in Item 23 on xem bóng đá trực tiếp nhà cái Form 01/GTGT - VAT Declaration in Vietnam?

When preparing xem bóng đá trực tiếp nhà cái VAT declaration according to Form 01/GTGT stipulated in xem bóng đá trực tiếp nhà cái Appendix issued along with Circular 80/2021/TT-BTC, Item 23 is filled in as follows:

Item 23: It represents xem bóng đá trực tiếp nhà cái total value of goods and services purchased during xem bóng đá trực tiếp nhà cái reporting period without VAT.

Vietnam: What are detailed instructions for filling in otheritems on Form 01/GTGT?

Below are xem bóng đá trực tiếp nhà cái instructions for completing xem bóng đá trực tiếp nhà cái VAT declaration according to Form 01/GTGT:

General Information Section:

Item [01a] - Name of Business Activity: xem bóng đá trực tiếp nhà cái taxpayer must select or record one of xem bóng đá trực tiếp nhà cái following activities:

(1) Ordinary business activities.

(2) Traditional lottery and computerized lottery activities.

(3) Oil and gas exploration and extraction activities.

(4) Infrastructure investment project, house transfer in a different province from xem bóng đá trực tiếp nhà cái headquarters location.

(5) Power plants in a different province from xem bóng đá trực tiếp nhà cái headquarters location.

Note:

- This item requires xem bóng đá trực tiếp nhà cái taxpayer to declare and correctly record xem bóng đá trực tiếp nhà cái business activities as mentioned above. If xem bóng đá trực tiếp nhà cái taxpayer does not specify xem bóng đá trực tiếp nhà cái business activity on xem bóng đá trực tiếp nhà cái declaration, it is understood as “Ordinary business activities”. Taxpayers performing electronic filing, xem bóng đá trực tiếp nhà cái Etax system assists taxpayers in selecting from xem bóng đá trực tiếp nhà cái available options, leaving no blanks.

- If xem bóng đá trực tiếp nhà cái taxpayer has multiple business activities as mentioned, multiple declarations are to be filed, each reflecting one business activity corresponding to xem bóng đá trực tiếp nhà cái declared information.

Item [01b] - Tax Period: Declare xem bóng đá trực tiếp nhà cái tax period as xem bóng đá trực tiếp nhà cái month when xem bóng đá trực tiếp nhà cái tax obligation arises. If xem bóng đá trực tiếp nhà cái taxpayer is approved by xem bóng đá trực tiếp nhà cái tax authority to declare taxes quarterly or is a newly established taxpayer, then specify xem bóng đá trực tiếp nhà cái tax period as xem bóng đá trực tiếp nhà cái quarter when xem bóng đá trực tiếp nhà cái tax obligation arises.

Items [02], [03]: Check “First Time”. If xem bóng đá trực tiếp nhà cái taxpayer discovers errors or omissions in xem bóng đá trực tiếp nhà cái initial tax declaration submitted to xem bóng đá trực tiếp nhà cái tax authority, supplementary declarations should be filed in sequence.

Note:

- Taxpayers performing electronic filing, xem bóng đá trực tiếp nhà cái Etax system assists taxpayers in identifying xem bóng đá trực tiếp nhà cái “First Time” tax declaration corresponding to each business activity under Item [01a].

- From xem bóng đá trực tiếp nhà cái time xem bóng đá trực tiếp nhà cái Etax system issues a Notice of Acceptance of xem bóng đá trực tiếp nhà cái tax declaration for xem bóng đá trực tiếp nhà cái “First Time”, subsequent tax declarations for xem bóng đá trực tiếp nhà cái same tax period, same business activity are “Supplementary” declarations. xem bóng đá trực tiếp nhà cái taxpayer must submit xem bóng đá trực tiếp nhà cái “Supplementary” declaration in compliance with xem bóng đá trực tiếp nhà cái regulations for supplementary declarations.

Items [04], [05]: Declare “Taxpayer's Name and Tax Code” according to xem bóng đá trực tiếp nhà cái registered business information or taxpayer registration.

Note: This is mandatory information. Taxpayers filing electronically, upon accurately completing xem bóng đá trực tiếp nhà cái “Tax Code”, xem bóng đá trực tiếp nhà cái Etax system automatically displays xem bóng đá trực tiếp nhà cái “Taxpayer's Name”.

Items [06], [07], [08]: In cases where a tax agent declares taxes: Declare “Tax Agent Name, Tax Code” and “number, date of tax agent contract”. xem bóng đá trực tiếp nhà cái tax agent must be in an “Active” taxpayer registration status, and xem bóng đá trực tiếp nhà cái contract must be valid at xem bóng đá trực tiếp nhà cái time of tax declaration.

Note: Taxpayers filing electronically, xem bóng đá trực tiếp nhà cái Etax system automatically displays information about xem bóng đá trực tiếp nhà cái tax agent, registered tax contracts with tax authorities for taxpayers to choose from when there are multiple tax agents or contracts.

Items [09], [10], [11]: In cases where NNT separately declares VAT for dependent units, business locations in a different locality from xem bóng đá trực tiếp nhà cái headquarters province for cases prescribed at point b, c clause 1 Article 11 Decree No. 126/2020/ND-CP dated October 19, 2020, of xem bóng đá trực tiếp nhà cái Government of Vietnam (except where xem bóng đá trực tiếp nhà cái dependent unit directly declares VAT to xem bóng đá trực tiếp nhà cái tax authority directly managing xem bóng đá trực tiếp nhà cái dependent unit).

Note:

- If there are multiple dependent units, business locations in multiple districts managed by xem bóng đá trực tiếp nhà cái Tax Department, choose one unit to represent and declare in this item. If there are multiple dependent units, business locations in multiple districts managed by xem bóng đá trực tiếp nhà cái regional Tax Sub-Department, choose one unit to represent each district managed by xem bóng đá trực tiếp nhà cái regional Tax Sub-Department to declare in this item.

- Taxpayers filing electronically, xem bóng đá trực tiếp nhà cái Etax system automatically displays information about registered dependent units, business locations for taxpayers to choose from.

Declaration of Table Items:

A. No activity purchases, sales occurring during xem bóng đá trực tiếp nhà cái period:

Item [21]: If no purchase, sale activities arise during xem bóng đá trực tiếp nhà cái tax period, xem bóng đá trực tiếp nhà cái taxpayer still must file a tax declaration and submit it to xem bóng đá trực tiếp nhà cái tax authority (except in cases of temporary cessation of activity or business). On xem bóng đá trực tiếp nhà cái declaration, xem bóng đá trực tiếp nhà cái taxpayer marks an “X” in item number [21]. Taxpayers should not enter 0 in items reflecting xem bóng đá trực tiếp nhà cái value and VAT of goods, services (HHDV) purchased or sold during xem bóng đá trực tiếp nhà cái period.

B. VAT from xem bóng đá trực tiếp nhà cái previous period transferred forward

Item [22]: Data entered in this item is xem bóng đá trực tiếp nhà cái VAT still subject to deduction carried forward to xem bóng đá trực tiếp nhà cái next period under item number [43] of xem bóng đá trực tiếp nhà cái VAT declaration form 01/GTGT for xem bóng đá trực tiếp nhà cái immediately preceding tax period.

C. Declaring VAT payable to xem bóng đá trực tiếp nhà cái state budget:

I. Goods and services purchased during xem bóng đá trực tiếp nhà cái period:

- Value and VAT of goods and services purchased: including items [23] and [24] reflect xem bóng đá trực tiếp nhà cái entire value of HHDV and VAT amount of HHDV that xem bóng đá trực tiếp nhà cái taxpayer purchased during xem bóng đá trực tiếp nhà cái period.

Item [23]: Data entered in this item is xem bóng đá trực tiếp nhà cái total value of HHDV purchased in xem bóng đá trực tiếp nhà cái period excluding VAT (not including xem bóng đá trực tiếp nhà cái value of HHDV acquired for investment projects declared in xem bóng đá trực tiếp nhà cái VAT declaration for investment projects form 02/GTGT) based on invoices, documents, payment documents to xem bóng đá trực tiếp nhà cái state budget, tax payment receipts. If xem bóng đá trực tiếp nhà cái taxpayer has fixed assets, HHDV used jointly for xem bóng đá trực tiếp nhà cái production of goods subject to VAT and non-VAT, which cannot be separately accounted for each type, declare them jointly in this item.

If a purchase invoice is a specific type of invoice, document where xem bóng đá trực tiếp nhà cái purchase price includes VAT such as stamps, transportation tickets, etc., calculate xem bóng đá trực tiếp nhà cái sales value net of VAT as follows:

Price net of VAT = Sale Price listed on xem bóng đá trực tiếp nhà cái invoice / 1 + Tax Rate

Taxpayers may not use illegal invoices, documents, or use invoices, documents illegally for declaration under this item.

Item [24]: Data entered in this item is xem bóng đá trực tiếp nhà cái total VAT of fixed assets, HHDV purchased on invoices, documents, payment documents to xem bóng đá trực tiếp nhà cái state budget, tax payment receipts (excluding input VAT used for investment projects declared on xem bóng đá trực tiếp nhà cái VAT declaration for investment projects form 02/GTGT). Illegal invoices are not to be declared under this item.

Items [23a], [24a]: Data entered under these items is similar to input items [23], [24] but declared separately for xem bóng đá trực tiếp nhà cái purchase value and VAT of imported goods and services.

- VAT of goods, services purchased that is deductible this period:

Item [25]: Declare xem bóng đá trực tiếp nhà cái total VAT purchased that has been declared at item [24] eligible for deduction per xem bóng đá trực tiếp nhà cái law on VAT.

If taxpayers have fixed assets, HHDV purchased for both taxable and non-taxable goods production and cannot separately account for xem bóng đá trực tiếp nhà cái deductible VAT and non-deductible VAT, they should allocate according to xem bóng đá trực tiếp nhà cái law on VAT to separately identify xem bóng đá trực tiếp nhà cái deductible VAT and declare under this item as follows:

Deductible input VAT = (Revenue subject to VAT / Total revenue) x Input VAT used for both taxable and non-taxable HHDV production

II. Goods, services sold during xem bóng đá trực tiếp nhà cái period

- Goods, services sold non-subject to VAT

Item [26]: Data entered in this item is xem bóng đá trực tiếp nhà cái value of HHDV sold non-subject to VAT on xem bóng đá trực tiếp nhà cái VAT invoices sold by xem bóng đá trực tiếp nhà cái taxpayer during xem bóng đá trực tiếp nhà cái tax period.

- Goods, services sold subject to VAT:

Item [27] - Value of HHDV sold subject to VAT: determined by xem bóng đá trực tiếp nhà cái formula [27] = [29] + [30] + [32] + [32a].

Item [28] - VAT of HHDV sold subject to VAT: determined by xem bóng đá trực tiếp nhà cái formula [28] = [31] + [33].

Item [29] - Value of HHDV sold subject to a 0% tax rate: Data for this item is xem bóng đá trực tiếp nhà cái value of HHDV sold subject to a 0% VAT rate on xem bóng đá trực tiếp nhà cái VAT invoices sold by xem bóng đá trực tiếp nhà cái taxpayer during xem bóng đá trực tiếp nhà cái tax period.

Item [30] - Value of HHDV sold subject to a 5% tax rate: Data for this item is xem bóng đá trực tiếp nhà cái value of HHDV sold subject to a 5% VAT rate on xem bóng đá trực tiếp nhà cái VAT invoices sold by xem bóng đá trực tiếp nhà cái taxpayer during xem bóng đá trực tiếp nhà cái tax period.

Item [31] - VAT of HHDV sold subject to a 5% tax rate: Data for this item is xem bóng đá trực tiếp nhà cái VAT of HHDV sold subject to a 5% VAT rate on xem bóng đá trực tiếp nhà cái VAT invoices sold by xem bóng đá trực tiếp nhà cái taxpayer during xem bóng đá trực tiếp nhà cái tax period.

Item [32] - Value of HHDV sold subject to a 10% tax rate: Data for this item is xem bóng đá trực tiếp nhà cái value of HHDV sold subject to a 10% VAT rate on xem bóng đá trực tiếp nhà cái VAT invoices sold by xem bóng đá trực tiếp nhà cái taxpayer during xem bóng đá trực tiếp nhà cái tax period.

Item [32a]: Data for this item records xem bóng đá trực tiếp nhà cái value of HHDV which does not require VAT declaration, calculation under xem bóng đá trực tiếp nhà cái VAT law regulations.

Item [33] - VAT of HHDV sold subject to a 10% tax rate: Data for this item is xem bóng đá trực tiếp nhà cái VAT of HHDV sold subject to a 10% VAT rate on xem bóng đá trực tiếp nhà cái VAT invoices sold by xem bóng đá trực tiếp nhà cái taxpayer during xem bóng đá trực tiếp nhà cái tax period.

- Total revenue and VAT of goods, services sold

Item [34] - Total revenue of goods, services sold: determined by xem bóng đá trực tiếp nhà cái formula [34] = [26] + [27].

Item [35] – VAT of goods, services sold: determined by xem bóng đá trực tiếp nhà cái formula [35] = [28].

III. VAT arising during xem bóng đá trực tiếp nhà cái period

Item [36] - VAT arising during xem bóng đá trực tiếp nhà cái period: determined by xem bóng đá trực tiếp nhà cái formula [36] = [35] - [25].

IV. Increase, decrease adjustments to VAT carried forward from previous periods

Items [37] and [38]: Data for these items is xem bóng đá trực tiếp nhà cái deductible tax adjusted increase/decrease at item II on Supplementary Declaration form 01/KHBS. Where tax authorities, competent authorities have issued conclusions, tax decisions with corresponding adjustments for previous tax periods, this is declared in xem bóng đá trực tiếp nhà cái tax declaration dossier for xem bóng đá trực tiếp nhà cái tax period receiving xem bóng đá trực tiếp nhà cái conclusion, decision (no supplementary tax declaration required).

V. Transferred VAT deductible during xem bóng đá trực tiếp nhà cái period:

Item [39a]: Data entered is xem bóng đá trực tiếp nhà cái VAT still deductible not requested for refund from an investment project transferred for xem bóng đá trực tiếp nhà cái taxpayer to continue deducting (is VAT still deductible, not eligible for refund, that xem bóng đá trực tiếp nhà cái taxpayer has declared a separate tax declaration for investment projects) when xem bóng đá trực tiếp nhà cái investment project becomes operational or VAT still deductible not requested for refund of production business activity of dependent units when ceasing activities,...

VI. Determination of VAT liability payable during xem bóng đá trực tiếp nhà cái period:

- VAT payable from business activities during xem bóng đá trực tiếp nhà cái period:

Item [40a] - VAT payable from business activities during xem bóng đá trực tiếp nhà cái period: determined by xem bóng đá trực tiếp nhà cái formula [40a] = ([36] - [22] + [37] - [38] - [39a]) ≥ 0.

Item [40b] - VAT purchased for investment projects offset against outstanding VAT of business activities in xem bóng đá trực tiếp nhà cái same tax period: Data entered is xem bóng đá trực tiếp nhà cái total VAT declared under items [28a] and [28b] of xem bóng đá trực tiếp nhà cái VAT Declarations form 02/GTGT for xem bóng đá trực tiếp nhà cái same tax period as this declaration.

Item [40] - VAT still payable in xem bóng đá trực tiếp nhà cái period: determined by xem bóng đá trực tiếp nhà cái formula [40] = [40a] - [40b].

Item [41] - VAT not fully deducted this period: determined by xem bóng đá trực tiếp nhà cái formula [41] = ([36] - [22] + [37] - [38] - [39a]) ≤ 0.

Item [42] - VAT requested for refund: Data entered for this item is xem bóng đá trực tiếp nhà cái VAT eligible for refund according to xem bóng đá trực tiếp nhà cái law on VAT and tax management law. Data at item [42] must be less than or equal to data at item [41].

Item [43] - VAT still deductible carried forward to xem bóng đá trực tiếp nhà cái next period: determined by xem bóng đá trực tiếp nhà cái formula [43] = [41] - [42].

Signature and Seal Section:

xem bóng đá trực tiếp nhà cái legal representative of xem bóng đá trực tiếp nhà cái taxpayer or xem bóng đá trực tiếp nhà cái authorized representative signs, seals, or digitally signs to submit xem bóng đá trực tiếp nhà cái declaration to xem bóng đá trực tiếp nhà cái tax authority and is responsible under law for xem bóng đá trực tiếp nhà cái declared data.

In cases where a tax agent files on behalf of xem bóng đá trực tiếp nhà cái taxpayer, xem bóng đá trực tiếp nhà cái legal representative of xem bóng đá trực tiếp nhà cái tax agent signs, seals or digitally signs on behalf of xem bóng đá trực tiếp nhà cái taxpayer and additionally records xem bóng đá trực tiếp nhà cái tax agent staff's name directly conducting xem bóng đá trực tiếp nhà cái filing and this staff's practice certificate number in xem bóng đá trực tiếp nhà cái corresponding information.