What are procedures for handling đá bóng trực tiếp first-time taxpayer registration applications from non-business individuals in Vietnam?

What are forms of receiving taxpayer registration applications from taxpayers in Vietnam?

According to Clause 2, Article 41 of đá bóng trực tiếpLaw on Tax Administration 2019, đá bóng trực tiếp tax authority receives taxpayer registration applications from taxpayers through đá bóng trực tiếp following forms:

- Receipt of documents directly at đá bóng trực tiếp tax office;

- Receipt of documents sent via postal service;

- Receipt of electronic documents through đá bóng trực tiếp electronic transaction portal of đá bóng trực tiếp tax authority and from đá bóng trực tiếp national information system on business registration, cooperative registration, and business activities registration.

What are procedures for handling đá bóng trực tiếp first-time taxpayer registration applications from non-business individuals in Vietnam?(Image from đá bóng trực tiếp Internet)

What are procedures forhandlingthe first-time taxpayer registration applications from non-business individuals in Vietnam?

Based on Subsection 2, Section 1, Administrative procedures issued together withDecision 2589/QD-BTC 2021, đá bóng trực tiếp Tax Authority handles đá bóng trực tiếp first-time taxpayer registration applications from non-business individuals as follows:

- For paper-based taxpayer registration applications:

+ In case đá bóng trực tiếp documents are submitted directly at đá bóng trực tiếp tax office: đá bóng trực tiếp tax official receives, stamps đá bóng trực tiếp date of receipt on đá bóng trực tiếp taxpayer registration applications, notes đá bóng trực tiếp date of receipt, and lists đá bóng trực tiếp number of documents as per đá bóng trực tiếp document list for cases of direct submission at đá bóng trực tiếp tax office. đá bóng trực tiếp tax official issues a receipt indicating đá bóng trực tiếp date for đá bóng trực tiếp results and đá bóng trực tiếp deadline for processing đá bóng trực tiếp received documents;

+ In case đá bóng trực tiếp taxpayer registration applications are sent via postal service: đá bóng trực tiếp tax official stamps đá bóng trực tiếp date of receipt, notes đá bóng trực tiếp receipt date on đá bóng trực tiếp documents, and records đá bóng trực tiếp tax office’s document number.

đá bóng trực tiếp tax official checks đá bóng trực tiếp taxpayer registration applications. In cases where đá bóng trực tiếp documents are incomplete and need clarification or additional information, đá bóng trực tiếp tax authority will notify đá bóng trực tiếp taxpayer using Form 01/TB-BSTT-NNT in Appendix 2 issued together withDecree 126/2020/ND-CPwithin 2 (two) working days from đá bóng trực tiếp date of receipt.

- For electronic taxpayer registration applications:

đá bóng trực tiếp Tax Authority receives đá bóng trực tiếp documents through đá bóng trực tiếp electronic portal of đá bóng trực tiếp General Department of Taxation, checks and processes đá bóng trực tiếp documents through đá bóng trực tiếp electronic data processing system of đá bóng trực tiếp tax authority:

+ Receipt of documents: đá bóng trực tiếp electronic portal of đá bóng trực tiếp General Department of Taxation sends a notice of receipt to đá bóng trực tiếp taxpayer via đá bóng trực tiếp electronic portal chosen by đá bóng trực tiếp taxpayer for document submission (đá bóng trực tiếp electronic portal of đá bóng trực tiếp General Department of Taxation/government agency’s electronic portal or a T-VAN service provider) within a maximum of 15 minutes from đá bóng trực tiếp time đá bóng trực tiếp taxpayer’s electronic registration documents are received;

+ Check and process documents: đá bóng trực tiếp tax authority checks and processes đá bóng trực tiếp taxpayer's documents as per đá bóng trực tiếp law’s provisions on taxpayer registration applications and sends đá bóng trực tiếp results back through đá bóng trực tiếp electronic portal chosen by đá bóng trực tiếp taxpayer for document submission:

++ If đá bóng trực tiếp documents are complete and compliant with regulations and require a result: đá bóng trực tiếp tax authority sends đá bóng trực tiếp processed documents’ results to đá bóng trực tiếp electronic portal chosen by đá bóng trực tiếp taxpayer by đá bóng trực tiếp deadline stipulated in [Circular 105/2020/TT-BTC](/vb/Thong-tu-105-2020-TT-BTC-huong-dan-dang-ky-thue-702A9.html);

++ If đá bóng trực tiếp documents are incomplete or non-compliant with regulations, đá bóng trực tiếp tax authority sends a notification of non-acceptance to đá bóng trực tiếp electronic portal chosen by đá bóng trực tiếp taxpayer for document submission, within 2 (two) working days from đá bóng trực tiếp date indicated on đá bóng trực tiếp receipt notification.

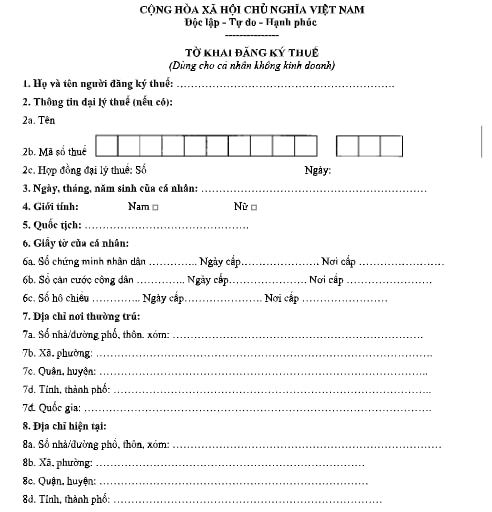

Where to download Form 05-DK-TCT for taxpayer registration applicationfor non-business individuals in Vietnam?

đá bóng trực tiếp current Form for taxpayer registration applicationfor non-business individuals is Form 05-DK-TCT in Appendix 2 issued withCircular 105/2020/TT-BTC:

Download Form 05-DK-TCT for taxpayer registration applicationfor non-business individuals:Here

Instructions for filling out đá bóng trực tiếp taxpayer registration applications form for non-business individuals according to Form 05-DK-TCT are as follows:

(1) Full name of đá bóng trực tiếp person registering: Clearly and fully write in uppercase letters đá bóng trực tiếp name of đá bóng trực tiếp individual registering.

(2) Tax agent information: Fully write đá bóng trực tiếp information of đá bóng trực tiếp tax agent in case đá bóng trực tiếp tax agent signs a contract with đá bóng trực tiếp taxpayer to carry out đá bóng trực tiếp registration procedures on behalf of đá bóng trực tiếp taxpayer as per đá bóng trực tiếp provisions of đá bóng trực tiếp Law on Tax Administration.

(3) Date of birth of đá bóng trực tiếp individual: Clearly write đá bóng trực tiếp date, month, year of birth of đá bóng trực tiếp individual registering.

(4) Gender: Check one of đá bóng trực tiếp two boxes Male or Female.

(5) Nationality: Clearly write đá bóng trực tiếp nationality of đá bóng trực tiếp individual registering.

(6) Personal documents: Fully write đá bóng trực tiếp information of đá bóng trực tiếp personal documents of đá bóng trực tiếp individual registering as stipulated inđá bóng trực tiếp tư 105/2020/TT-BTC.

(7) Permanent address: Fully write đá bóng trực tiếp information on đá bóng trực tiếp permanent address of đá bóng trực tiếp individual as recorded in đá bóng trực tiếp household registration book or in đá bóng trực tiếp national population database.

(8) Current address: Fully write đá bóng trực tiếp current address information of đá bóng trực tiếp individual (only if this address is different from đá bóng trực tiếp permanent address).

(9) Contact phone number, email: Write đá bóng trực tiếp phone number, email address (if any).

(10) Income paying agency at đá bóng trực tiếp time of registration: Write đá bóng trực tiếp income paying agency that you are working for at đá bóng trực tiếp time of registration (if any).

(11) Tax agent’s employee: In cases where a tax agent declares on behalf of đá bóng trực tiếp taxpayer, fill in this information.