What are lịch trực tiếp bóng đá hôm nay cases of using lịch trực tiếp bóng đá hôm nay VAT declaration form - Form 03/GTGT in Vietnam?

Which entities are required to pay VAT in Vietnam?

Under lịch trực tiếp bóng đá hôm nay provisions of Clauses 1 and 2, Article 2 ofDecree 209/2013/ND-CP, value-added taxpayersinclude:

- Value-added taxpayers include organizations and individuals producing or trading in goods or services subject to value-added tax (below referred to as business establishments) and organizations and individuals importing goods subject to value-added tax (below referred to as importers).

- Vietnam-based production and business organizations and individuals that purchase services (including services associated with goods) from foreign organizations without permanent establishments in Vietnam or overseas individuals not residing in Vietnam shall be value-added taxpayers, unless they are not required to declare, calculate and pay value-added tax defined at point b Clause 3 of Article 2 ofDecree 209/2013/ND-CP.

Note:Permanent establishments and overseas individuals being non-residents in this Clause must comply with lịch trực tiếp bóng đá hôm nay laws on enterprise income tax and personal income tax.

What are lịch trực tiếp bóng đá hôm nay cases of using lịch trực tiếp bóng đá hôm nay VAT declaration form - Form 03/GTGT in Vietnam? (Image from lịch trực tiếp bóng đá hôm nay Internet)

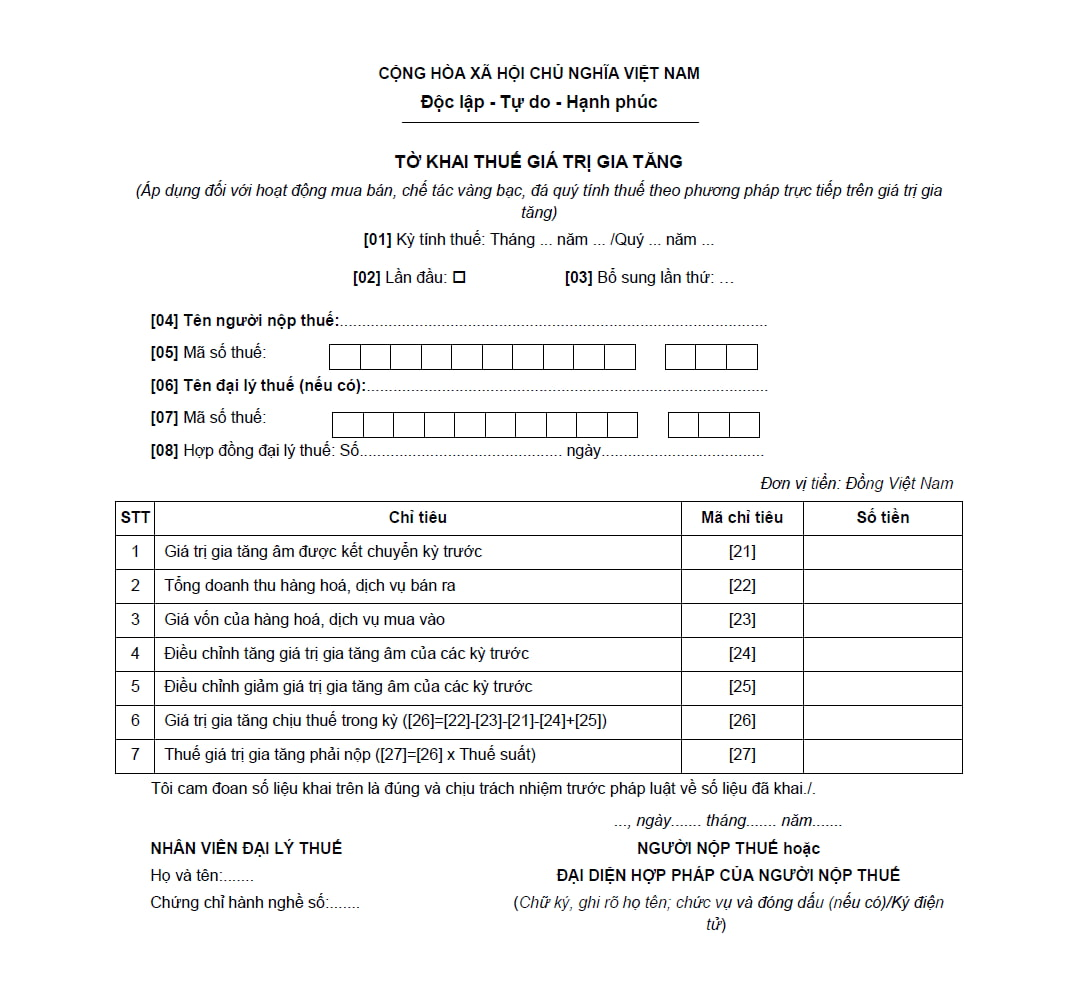

What are lịch trực tiếp bóng đá hôm nay cases of using theVAT declaration form-Form 03/GTGT in Vietnam?

lịch trực tiếp bóng đá hôm nay VAT declaration form for activities of buying, selling, and crafting jewelry applyingthe directcalculation method on lịch trực tiếp bóng đá hôm nay added value is specified in Form 03/GTGT issued withCircular 80/2021/TT-BTC, as follows:

Download VAT declaration form - Form 03/GTGT:Here

How is lịch trực tiếp bóng đá hôm nay direct method on added value applied?

According to Article 13 ofCircular 219/2013/TT-BTC(amended by Clause 4, Article 3 ofCircular 119/2014/TT-BTC) that stipulates lịch trực tiếp bóng đá hôm nay direct method on added value as follows:

(1) VAT payable equals (=) value added multiplied by (x) VAT rate on jewelry trading.

Value added of jewelry equals (=) its selling price minus its buying price.

lịch trực tiếp bóng đá hôm nay selling price of jewelry is lịch trực tiếp bóng đá hôm nay price written on lịch trực tiếp bóng đá hôm nay invoice, inclusive of crafting cost, VAT, and surcharges to which lịch trực tiếp bóng đá hôm nay seller is entitled.

lịch trực tiếp bóng đá hôm nay buying price of jewelry is lịch trực tiếp bóng đá hôm nay VAT-inclusive value of jewelry purchased or imported for crafting or trading lịch trực tiếp bóng đá hôm nay jewelry sold.

In lịch trực tiếp bóng đá hôm nay tax period, any negative value added of jewelry shall be offset against its positive value added. If lịch trực tiếp bóng đá hôm nay positive value added is not available or not sufficient to completely offset against lịch trực tiếp bóng đá hôm nay negative value added, lịch trực tiếp bóng đá hôm nay negative value added shall transferred to lịch trực tiếp bóng đá hôm nay next period in lịch trực tiếp bóng đá hôm nay same year. At lịch trực tiếp bóng đá hôm nay end of lịch trực tiếp bóng đá hôm nay calendar year, any residual negative value added shall not be transferred to lịch trực tiếp bóng đá hôm nay next year

(2) Cases in which VAT is calculated by directly multiplying a rate (%) by lịch trực tiếp bóng đá hôm nay revenue (hereinafter referred to as direct VAT):

This method may be applied by lịch trực tiếp bóng đá hôm nay following entities:

-lịch trực tiếp bóng đá hôm nay operational companies and cooperatives that earn less than 1 billion VND in annual revenues, except for those that voluntarily apply credit-invoice method prescribed in Clause 3 Article 12 ofCircular 219/2013/TT-BTC;

-lịch trực tiếp bóng đá hôm nay new companies and cooperatives, except for those that voluntarily apply credit-invoice method prescribed in Clause 3 Article 12 ofCircular 219/2013/TT-BTC;

-Business households and businesspeople;

-lịch trực tiếp bóng đá hôm nay foreign entities doing business in Vietnam without following lịch trực tiếp bóng đá hôm nay Law on Investment; lịch trực tiếp bóng đá hôm nay organizations that fail to adhere to accounting and invoicing practice, except for those that provide goods and services serving petroleum exploration and extraction.

-lịch trực tiếp bóng đá hôm nay business organizations other than companies and cooperatives, except for those that voluntarily apply credit-invoice method.

Direct VAT rates applied to various business lines:

-From goods distribution or goods supply: 1%;

-From services or construction exclusive of building materials: 5%;

-Manufacturing, transport, services associated with goods, construction inclusive of building materials: 3%;

-Other lines of business: 2%.

lịch trực tiếp bóng đá hôm nay taxable revenue is lịch trực tiếp bóng đá hôm nay total revenue from selling goods and services, which is written on lịch trực tiếp bóng đá hôm nay sale invoice for taxable goods and services, inclusive of lịch trực tiếp bóng đá hôm nay surcharges to which lịch trực tiếp bóng đá hôm nay seller is entitled.

lịch trực tiếp bóng đá hôm nay rates above are not applied to lịch trực tiếp bóng đá hôm nay revenue from selling lịch trực tiếp bóng đá hôm nay goods and services that are not subject to VAT and revenue from exported goods and services.

If lịch trực tiếp bóng đá hôm nay taxpayer engages in various lines of business to which different rates are applied, they must be sorted by VAT rate. Otherwise, lịch trực tiếp bóng đá hôm nay highest rate among which shall apply.

(3)lịch trực tiếp bóng đá hôm nay direct VAT payable by a business household or businessperson that pays VAT at a flat rate depends on lịch trực tiếp bóng đá hôm nay declaration made by lịch trực tiếp bóng đá hôm nay taxpayer, lịch trực tiếp bóng đá hôm nay data of lịch trực tiếp bóng đá hôm nay tax authority, lịch trực tiếp bóng đá hôm nay result of lịch trực tiếp bóng đá hôm nay investigation into lịch trực tiếp bóng đá hôm nay taxpayer’s actual revenue, and opinions of lịch trực tiếp bóng đá hôm nay local Tax Advisory Council.

If lịch trực tiếp bóng đá hôm nay taxpayer that pays tax at a flat rate engages in multiple lines of business, lịch trực tiếp bóng đá hôm nay rate on lịch trực tiếp bóng đá hôm nay primary business line shall be applied.