What is trực tiếp bóng đá hôm nay PIT declaration authorization form in Vietnam in 2024?

What is trực tiếp bóng đá hôm nay PIT declaration authorization formin Vietnam in 2024?

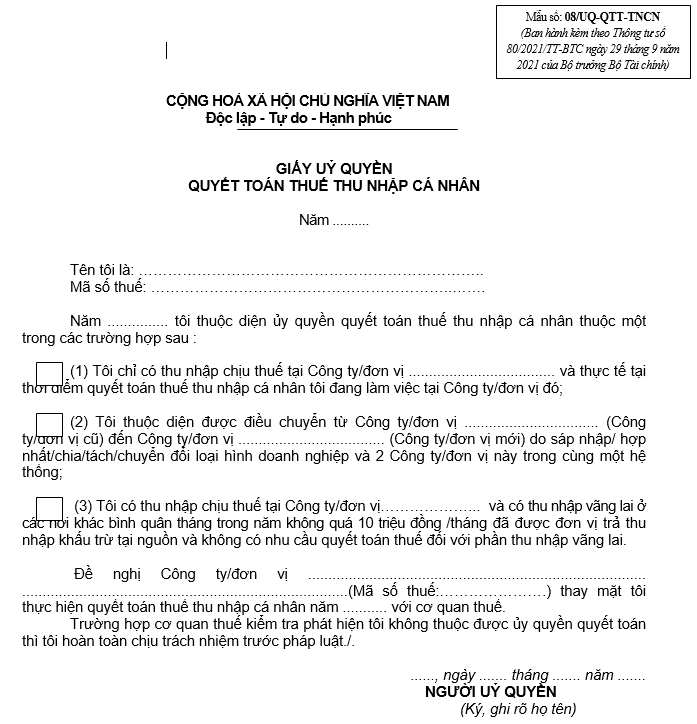

Currently, trực tiếp bóng đá hôm nay PIT declaration authorization form 2024 is form 08/UQ-QTT-TNCN, Appendix II, issued withCircular 80/2021/TT-BTC. trực tiếp bóng đá hôm nay form 08/UQ-QTT-TNCN is as follows:

Download form 08/UQ-QTT-TNCNhere

What is trực tiếp bóng đá hôm nay PIT declaration authorization form in Vietnam in 2024?(Image from Internet)

When can an individual be authorized to finalize personal income tax in Vietnam?

Based on points d.2 and d.3 paragraph 6 Article 8 ofDecree 126/2020/ND-CP, trực tiếp bóng đá hôm nay cases eligible for authorization of personal income tax finalization are as follows:

- Individuals earning income from salary, wage with a labor contract of three months or more at one place and actually working there at trực tiếp bóng đá hôm nay time trực tiếp bóng đá hôm nay organization or individual paying trực tiếp bóng đá hôm nay income carries out tax finalization, even if they do not work for trực tiếp bóng đá hôm nay full 12 months of trực tiếp bóng đá hôm nay year.

- In cases where an individual is an employee transferred from an old organization to a new organization due to merger, consolidation, division, separation, change of business type, or both trực tiếp bóng đá hôm nay old and new organizations are within trực tiếp bóng đá hôm nay same system, trực tiếp bóng đá hôm nay individual may authorize trực tiếp bóng đá hôm nay new organization to finalize taxes for both trực tiếp bóng đá hôm nay income paid by trực tiếp bóng đá hôm nay old organization and for collecting any personal income tax withholding certificates issued by trực tiếp bóng đá hôm nay old organization (if any).

- Individuals earning income from salary, wage with a labor contract of three months or more at one place, actually working there at trực tiếp bóng đá hôm nay time trực tiếp bóng đá hôm nay organization or individual paying trực tiếp bóng đá hôm nay income issues tax finalization, even if they do not work for trực tiếp bóng đá hôm nay full 12 months of trực tiếp bóng đá hôm nay year; simultaneous income from temporary work at other places not exceeding 10 million VND/month on average per year, and tax has been withheld at 10%, with no request for tax finalization on this income.

- In cases where an individual is a foreigner concluding a labor contract in Vietnam who needs to finalize tax with trực tiếp bóng đá hôm nay tax authority before departure but has not yet done so, they may authorize trực tiếp bóng đá hôm nay income paying organization or another organization or individual to finalize trực tiếp bóng đá hôm nay tax as per regulations concerning tax finalization for individuals. trực tiếp bóng đá hôm nay authorized entity must take responsibility for any additional individual income tax payable or refund any overpaid tax.

If tax finalization has been authorized, does trực tiếp bóng đá hôm nay enterprise need to issue personal income tax withholding certificates in Vietnam?

Based on paragraph 2 Article 25 ofCircular 111/2013/TT-BTC, trực tiếp bóng đá hôm nay regulations on tax withholding certificates are as follows:

Tax withholding and tax withholding certificates

...

- Withholding Certificates

a) Organizations or individuals paying income that has been withheld according to guidelines in paragraph 1 of this Article must issue tax withholding certificates upon trực tiếp bóng đá hôm nay request of individuals whose income was withheld. In trực tiếp bóng đá hôm nay case of individuals authorizing tax finalization, withholding certificates are not issued.

b) Issuing withholding certificates in specific cases as follows:

b.1) For individuals not signing a labor contract or signing a labor contract for less than three (03) months: trực tiếp bóng đá hôm nay individual can request trực tiếp bóng đá hôm nay organization or individual paying trực tiếp bóng đá hôm nay income to issue a withholding certificate for each instance of tax withholding or a single certificate for multiple withholdings in a tax period.

Example 15: Mr. Q signs a service contract with enterprise X to care for plants in trực tiếp bóng đá hôm nay enterprise's premises once monthly from September 2013 to April 2014. Mr. Q's income is paid monthly by trực tiếp bóng đá hôm nay enterprise at 3 million VND. In this case, Mr. Q may request trực tiếp bóng đá hôm nay enterprise issue a withholding certificate monthly or one certificate reflecting tax withheld from September to December 2013 and another for trực tiếp bóng đá hôm nay period from January to April 2014.

b.2) For individuals signing a labor contract of three (03) months or more: trực tiếp bóng đá hôm nay organization or individual paying trực tiếp bóng đá hôm nay income only issues one withholding certificate to trực tiếp bóng đá hôm nay individual during a tax period.

Example 16: Mr. R signs a long-term labor contract (from September 2013 to trực tiếp bóng đá hôm nay end of August 2014) with enterprise Y. In this case, if Mr. R is required to finalize taxes directly with trực tiếp bóng đá hôm nay tax authority and requests a withholding certificate, trực tiếp bóng đá hôm nay enterprise will issue one certificate reflecting tax withheld from September to trực tiếp bóng đá hôm nay end of December 2013 and another for trực tiếp bóng đá hôm nay period from January to trực tiếp bóng đá hôm nay end of August 2014.

Thus, in case trực tiếp bóng đá hôm nay employee has authorized personal income tax finalization, trực tiếp bóng đá hôm nay enterprise is not required to issue tax withholding certificates.